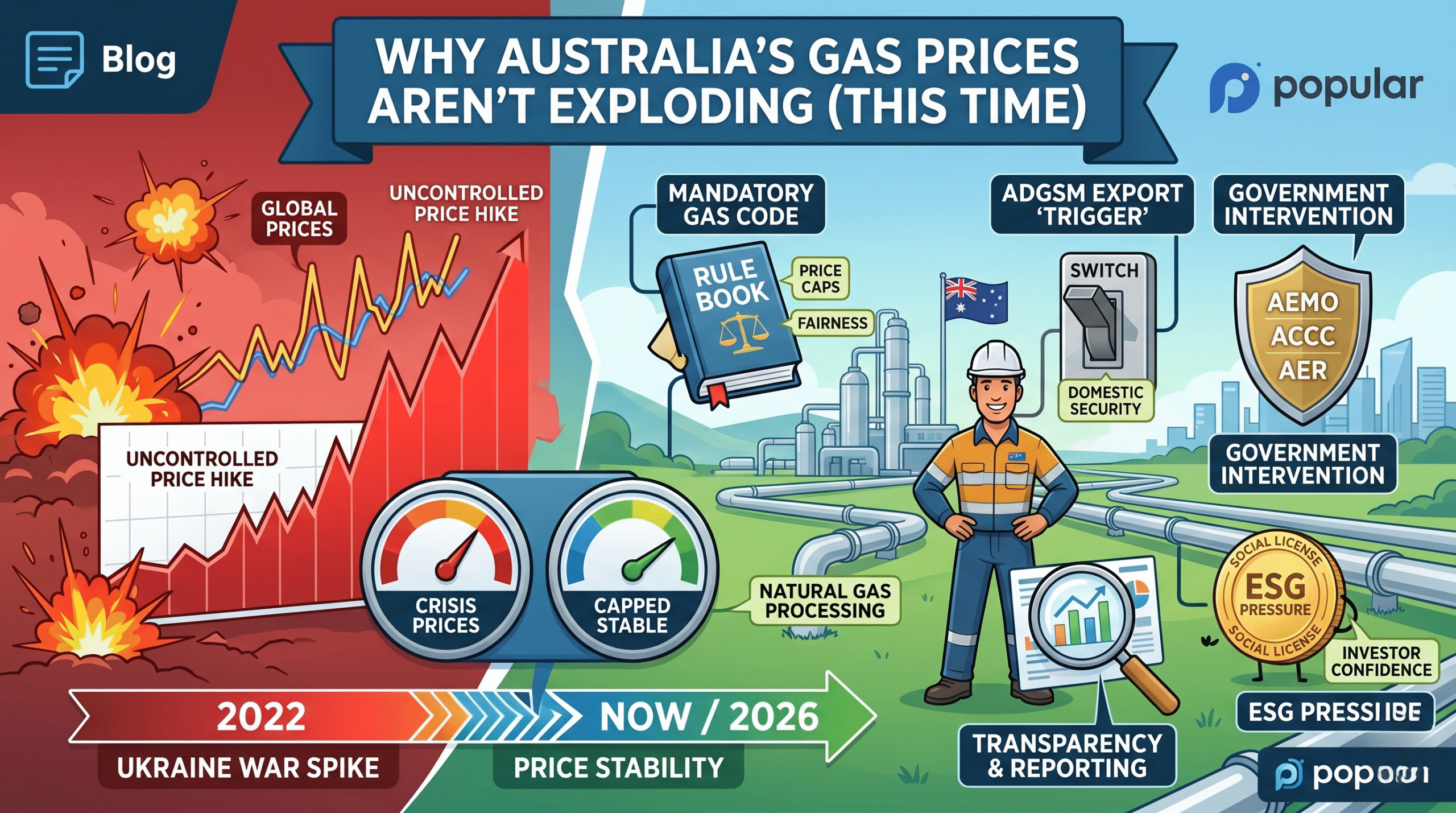

Remember 2022? It was a rough year for anyone paying an energy bill. When the war in Ukraine broke out, global energy markets went into a tailspin. In Australia—despite being one of the world’s largest gas exporters—domestic prices skyrocketed. We were essentially paying “war prices” for gas dug up in our own backyard.

Fast forward to April 2026, and the world is still a messy place. We’ve seen fresh conflicts in the Middle East and ongoing global instability. Yet, interestingly, the “Big Gas” producers in Australia haven’t gone on another price-hiking spree.

Why the change of heart? Is it corporate kindness? (Spoilers: No). It’s actually a mix of heavy-handed government intervention, new “rules of the road,” and a shift in how global markets are moving.

Let’s break it down into simple terms.

1. The “Gas Code of Conduct” (The New Rulebook)

The biggest reason for the price stability is that the Australian government stopped asking nicely and started demanding fairness. After the 2022 spike, the government introduced a Mandatory Gas Code of Conduct.

Think of this as a referee who finally stepped onto the field. This code includes a price cap (initially set around $12 per gigajoule) that prevents producers from charging whatever they want. While there are exemptions for producers who commit to supplying the domestic market, the “threat” of the code keeps prices anchored.

2. The ADGSM: The “Big Stick” in the Closet

Australia has a safety valve called the Australian Domestic Gas Security Mechanism (ADGSM), often nicknamed the “gas trigger.”

In 2022, this mechanism was a bit clunky. Since then, it has been sharpened. The Minister for Resources now has the power to look at the upcoming quarter (like the recent notice for Q3 2026) and say: “If there isn’t enough gas for Aussies, you can’t export your extra supply.” Because producers don’t want their lucrative export deals cancelled, they make sure to leave enough gas in the domestic “tank” to keep the Minister happy.

3. The “Heads of Agreement” (The Pinky Swear)

The government also secured a “Heads of Agreement” with the major LNG (Liquefied Natural Gas) exporters in Queensland. This is basically a formal promise that they will offer uncontracted gas to the domestic market first, and at reasonable prices, before they try to sell it overseas for a massive profit.

In the past, producers would see high prices in Europe and ship every spare molecule of gas there. Now, they are legally and politically bound to check if Australia needs it first.

4. A “Cooler” International Market

While the world is still tense, the global gas market isn’t in the same “panic mode” it was in 2022.

- Inventory is higher: Europe and Asia have gotten better at storing gas.

- The US is pumping: The United States has ramped up its own LNG exports, taking some of the pressure off Australian supply.

- Prices have eased: Even though there are spikes, the baseline international price is lower than the record-breaking peaks seen at the start of the Ukraine war.

5. Transparency is Finally Here

In the old days, the gas market was like a secret club. Only the big producers knew how much gas was available and what the real price was.

As of 2025 and 2026, the ACCC (Australian Competition and Consumer Commission) and the AER (Australian Energy Regulator) have much better “eyes” on the market. They release regular reports showing exactly where the gas is and what producers are charging. When everyone can see the data, it’s much harder for producers to claim there’s a “shortage” to justify a price hike.

6. The Long-Term Shift: Moving Away from Gas

Finally, there’s a change in demand. Many Australian households and businesses are switching to electricity (induction cooktops, heat pumps) or investing in renewables. As domestic demand slowly starts to peak or decline in certain sectors, producers realize they can’t push prices too high without accelerating the “death” of their own market.

7. The “Domestic First” Cultural Shift (ESG Pressures)

In 2022, gas companies faced a massive public relations nightmare. They were reporting record profits while Australian pensioners couldn’t afford to turn on their heaters. Since then, ESG (Environmental, Social, and Governance) standards have become a massive deal for investors.

- The Pressure: Shareholders are now demanding that these companies maintain a “Social License to Operate.”

- The Result: If a company like Woodside or Santos is seen as “gouging” Aussie mums and dads, it risks heavy government taxes (like a Windfall Tax) and divestment from big superannuation funds. They’ve learned that a short-term price hike isn’t worth a long-term political war.

8. Increased Storage Capacity (The “Battery” for Gas)

One of Australia’s biggest weaknesses in 2022 was that we didn’t have enough places to keep gas for a rainy day.

- Better Infrastructure: Over the last few years, there has been a push to increase gas storage facilities (like the Iona underground storage in Victoria).

- Smoothing the Peaks: Think of storage like a water tank. By filling these tanks when demand is low, we can release the gas when it gets cold in winter. This prevents the “panic buying” that usually allows producers to jack up prices during a cold snap.

9. The Rise of “Firming” Renewables

The way we use gas in Australia is changing. We use it less for “base load” power and more for “firming”—which means turning on gas plants only when the sun isn’t shining or the wind isn’t blowing.

- Less Constant Demand: Because big batteries (like the Waratah Super Battery) are now coming online, we don’t need to burn gas 24/7.

- Market Impact: When demand is flexible rather than constant, gas producers lose their “hostage grip” on the market. They can’t demand high prices because the market can often just wait for the wind to pick up instead.

10. Strategic Negotiation by Large Industrial Users

In 2022, manufacturing plants (brick makers, chemical plants, glass factories) were caught off guard with “take it or leave it” contracts.

- Group Buying: Large industrial users have become smarter. They are now forming buying groups and negotiating long-term contracts directly with smaller, Tier-2 gas producers.

- Breaking the Monopoly: This competition from smaller producers (who are exempt from some of the bigger export rules) forces the “Big 3” producers to keep their domestic offers competitive to avoid losing market share entirely.

11. The Shadow of the “Super Profits Tax”

There has been constant talk in Canberra about a Petroleum Resource Rent Tax (PRRT) reform.

- The Threat: The government has basically sent a message to the gas industry: “If you play fair and keep prices low, we won’t touch your tax rate. If you start price-gouging again, we will tax your profits into the ground.”

- The Deterrent: This “tax threat” is perhaps the most effective tool the Treasurer has. It keeps the gas giants on their best behavior because a new tax would cost them billions more than they would make from a temporary price hike.

12. Improved East-Coast Interconnectors

In the past, gas was often “trapped” in certain states. You might have plenty of gas in Queensland but a shortage in New South Wales, leading to local price spikes.

- Better Pipelines: Improvements to the Southwest Queensland Pipeline and other interconnectors now allow gas to flow more freely across state lines.

- National Price Levelling: When gas can move easily from where it’s found to where it’s needed, it prevents “bottlenecks” that producers previously used as an excuse to raise prices in specific regions.